The most popular mode of undertaking Corporate Social Responsibility (CSR) since 2014 has been through nonprofit organisations. Forty-three percent of all CSR funds spent in the last four years were disbursed through these entities.

In 2018, the Ministry of Corporate Affairs (MCA) convened a High-Level Committee (HLC) on CSR to review the effectiveness of Section 135 of the Companies Act, 2013—which makes CSR mandatory for companies above a certain level of net worth—and suggest changes. As part of this effort, ATE Chandra Foundation partnered with Samhita Social Ventures to conduct a national consultation with 320 nonprofits1 to understand their experiences with and views on accessing CSR funds and implementing CSR projects, which led to some interesting insights.

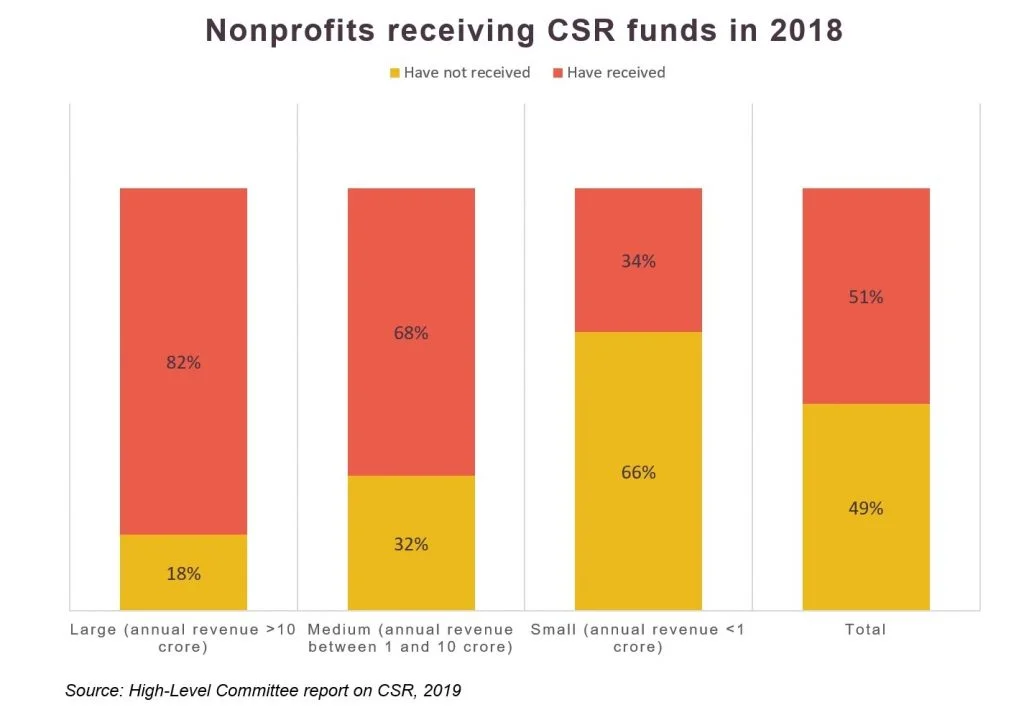

Most nonprofits expressed a desire to benefit from CSR opportunities. But one out of two nonprofits surveyed had not received any CSR funding in the year before the consultation (2018). The survey responses suggested that the size of the nonprofit had a bearing on its ability to raise CSR funds: a third of the small nonprofits (with annual revenue less than INR 1 crore) received CSR funding in the previous year, compared to more than 80 percent of the large nonprofits (with annual revenue more than INR 10 crore).

Part of the reason why this is the case has to do with donors. Most institutional funders—individuals, foundations, or CSR—require of their grantees a well-established track record, organisational systems and processes, and the ability to measure and report impact, all of which might be difficult for small nonprofits to achieve.

Anecdotal evidence showed that very few CSR funders provide support to put in place the very systems and processes that they require.

Additionally, anecdotal evidence gathered during the consultation showed that very few CSR funders provide support to put in place the very systems and processes that they require, guided by a misplaced notion of using lower overhead costs as an indicator of efficiency. This results in a vicious cycle, where smaller nonprofits do not have enough funding to adopt systems and processes required to secure more institutional funding.

Nonprofits registered in central states (Madhya Pradesh, Chhattisgarh, Uttar Pradesh, Jharkhand, and Bihar) received at least 40 percent less CSR funding as compared to other regions.2 In fact, 46 percent of nonprofits reported their geographical location as a reason for not receiving CSR funds. This finding aligns with the generally known geographical skew in CSR, driven in part by subsection 5 of Section 135 that states that “the company shall give preference to the local area,” along with the 2018 circular from the Ministry of Corporate Affairs reiterating that this provision be followed in both letter and spirit.

Related article: Why funders must support leadership development in nonprofits

Schedule VII of Section 135 lists down the activities that companies may support with CSR funds. It includes a range of activities, from ending hunger and empowering women, to supporting government programmes. But approximately one out of three nonprofits in the survey believed that Schedule VII has left out important issues, such as those related to Adivasis and other vulnerable communities, child protection, urban planning, and so on, and that companies were interpreting the schedule narrowly.

Similarly, under the current popular interpretation of the Act, critical building blocks for the sector, including capacity building, research, and advocacy, are being neglected. Eighty-two percent of nonprofits reported that capacity building should be explicitly included under Schedule VII, and 87 percent voiced the same for research and advocacy.

The top three barriers, as identified by the nonprofits in the consultation, include lack of information on CSR opportunities, lack of understanding of CSR requirements on the nonprofits’ part, and geography. These were reported by small and large nonprofits alike, though the smaller nonprofits were more likely to face these.

Interestingly, even though the data suggested a clear preference for larger nonprofits, as mentioned above, nonprofits themselves did not perceive size and scale as a critical barrier, possibly an indication of lack of clarity regarding the functioning of CSR. Another important barrier that was stated was the trust deficit between companies and nonprofits, perhaps caused by a lack of understanding and appreciation for each other’s contexts and challenges, and exacerbated by the absence of forums that address this deficit in a constructive manner.

Apart from these, an overwhelming majority (94 percent) of the nonprofits reported facing challenges in contacting companies for CSR funds.

Two out of five nonprofits that received CSR funding in the year before the survey (2018) reported facing challenges in implementing CSR projects. The most reported challenge was a lack of long-term commitment from companies, causing uncertainty and instability among nonprofits. This was followed by a perceived lack of understanding on the part of companies about social issues and solutions, and an emphasis on achieving targets. Other challenges included delayed deployment of funds, not addressing issues across the value chain of the cause area, and not having a funding buffer when CSR support is withdrawn, nor a window of time within which the nonprofit might find another source of revenue.

When asked about the usefulness of corporate employee engagement programmes that involve volunteering at nonprofits, the verdict was split. Fifty-three percent of the nonprofits thought it was always or very often beneficial, especially when a company’s employee talent pool in technology, marketing, fundraising, or networking complemented the nonprofit’s work in a planned and effective way. On the other hand, 47 percent of the nonprofits were uncertain of the value of employee engagement programmes, because they felt that arranging for employee volunteering increased costs, was time-intensive, and was of little help as corporate volunteers often lacked the understanding or the soft skills required to work with communities.

The nonprofits in the consultation expressed concerns about CSR spending by Public Sector Undertakings (PSUs). They felt that CSR spending by PSUs was largely driven by government pressure and agendas, and was not strategic or impactful, given the excessive focus on infrastructure. Nonprofits found it difficult to approach PSUs for CSR, due to their bureaucratic processes and lack of transparency. Many PSUs themselves seemed reluctant to partner with nonprofits and preferred government agencies.

CSR by PSUs was largely seen as a wasted opportunity in need of revision, especially given their regional footprint and substantial budgets.

Some nonprofits also shared instances where they, despite being not-for-profit in nature, had to go through a tendering process similar to private vendors, with requirements such as offering a performance guarantee. While a few nonprofits did understand the constraints faced by PSUs in terms of the scrutiny and audit requirements, CSR by PSUs was largely seen as a wasted opportunity in need of revision, especially given their regional footprint and substantial budgets.

Related article: Five Cs to better employee engagement

Despite the concerns and challenges around access to CSR, most nonprofits were optimistic about tapping into this opportunity. To enable that, the HLC made several recommendations to the government, which include:

Beyond regulatory structures, it is critical to recognise the importance of empathy and ongoing dialogue among partners in accessing the full potential of collaboration around CSR. Therefore, strengthening relationships and building trust between the corporate and civil society sectors should remain a priority and a collective responsibility for the Indian development ecosystem.

—

Know more