In April 2025, a petitioner approached the Supreme Court of India because she could not independently access basic banking services since every digital option available to her was inaccessible to her as a person with disability. The court’s response was unambiguous: Digital accessibility for persons with disabilities is a constitutional right, not a design preference. This was a landmark judgment. What it revealed, almost as a side note, was that in a country celebrating a decade of the fintech revolution, tens of millions of people have been locked out the entire time.

India’s fintech story is one of the most celebrated in the world. The Unified Payments Interface processed over 19 billion transactions in November 2025 alone. Jan Dhan accounts brought hundreds of millions of previously unbanked citizens into the formal financial system. By almost every metric, India’s digital financial inclusion project has been a remarkable success. However, it has not included everyone.

It is assumed that every user can see a screen clearly, hear a voice prompt, hold a phone steady, complete a blinking gesture for a liveness check (a test that confirms a real person is present), or display a PAN card to a camera. That every user navigates apps designed for fingers with full dexterity and eyes with full sight. For India’s 50 to 80 million persons with disabilities, this assumption poses a huge barrier in access to banking services.

Built for one kind of body

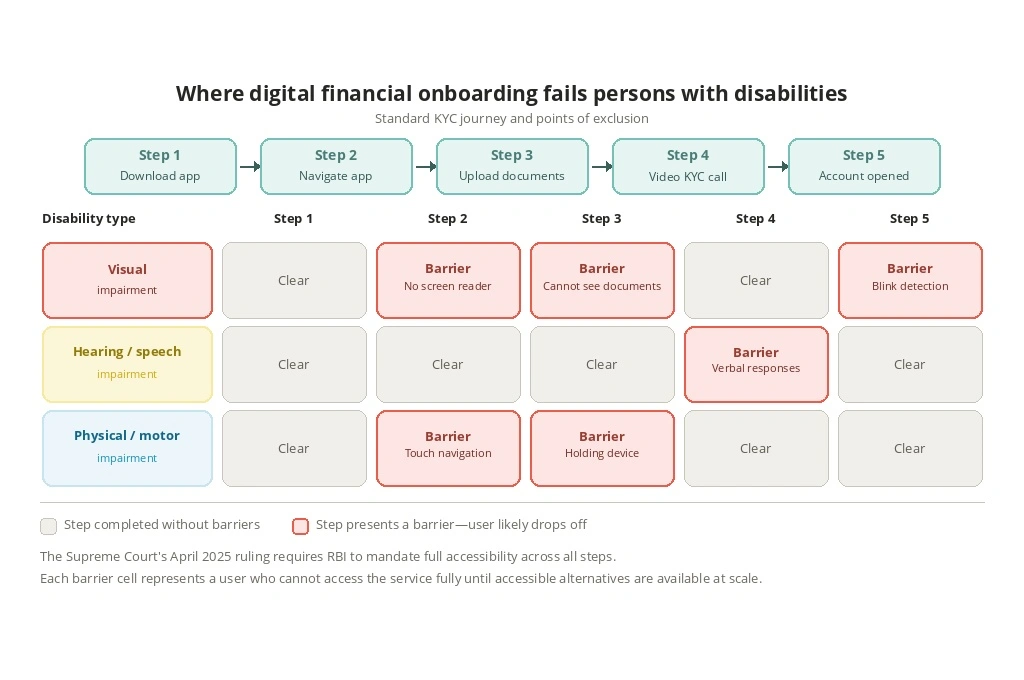

Consider what opening a bank account or accessing a digital loan requires today. Most regulated entities use Video-based Customer Identification Process—a live video verification process that banks and fintechs use to confirm a customer’s identity remotely—as their primary Know Your Customer (KYC) mechanism. The process typically requires a user to blink on command, hold up a physical document to the camera, and respond verbally to an agent’s questions. For a person with visual impairment, a physical disability affecting hand movement, speech impairment, or hearing loss, each of these steps is either difficult or impossible to complete independently.

This is a structural design failure affecting one of the largest populations of disabled persons worldwide, a majority of whom are working-age adults—legally eligible for and actively seeking financial services.

Banking apps and fintech platforms routinely lack screen reader compatibility.

The problem does not end at onboarding. As accessibility audits and user research consistently document, banking apps and fintech platforms routinely lack screen reader compatibility (software that reads out on-screen text aloud for users with visual impairments), voice navigation, high contrast display options, and gesture-based alternatives for users who cannot interact with touch interfaces in standard ways. Password reset flows, transaction authentication, and complaint resolution mechanisms all carry the design assumption that the person on the other end of the device is able-bodied and tech-literate in a very specific way.

When that assumption fails, users with disabilities must choose between giving up on the service entirely or handing their phone, their credentials, and their financial autonomy to a caregiver. Neither option is acceptable in a system that claims to be building financial inclusion.

What makes this exclusion particularly difficult to address is that it is largely invisible in the data. Financial institutions do not collect data on whether their users have disabilities, so there is no internal evidence of a problem to act on. There is no drop-off rate at onboarding attributed to disability, nor is there a complaint category for inaccessible interfaces. A fintech entity can genuinely believe it is building an interface for everyone while having no mechanism to discover that an entire category of users has quietly given up and walked away. Invisibility in the data produces invisibility in the product roadmap.

The law has caught up, but the industry has not

The Pragya Prasun and Amar Jain versus Union of India judgment ruled that digital accessibility is a fundamental right under Articles 14, 19, and 21 of the Constitution, guaranteeing equality, freedom of expression, and the right to life and dignity. The court directed the Reserve Bank of India to issue clear, time-bound instructions to all regulated entities, including banks, non-banking financial companies, and fintech platforms, to make their services fully accessible across the disability spectrum.

The RBI had already taken a preliminary step with its 2024 guidelines on digital payment access for persons with disabilities. These guidelines directed regulated entities to provide accessible alternatives for persons with visual, hearing, speech, and motor impairments and to establish dedicated grievance mechanisms for accessibility-related barriers. The Fintech Association for Consumer Empowerment (FACE), which functions as a self-regulatory organisation for fintech organisations, has submitted a detailed framework proposing inclusive onboarding alternatives, universal design standards, caregiver-assisted consent protocols, and phased implementation timelines.

Implementation requires the industry to have the will, the knowledge, and the incentive to move from policy commitments to actual product change. India’s Rights of Persons with Disabilities Act has been in force since 2016, yet financial services remained a grey area until this judgment, a gap that reflects how far legal mandate can sit from ground-level implementation.

Why this is an opportunity, not a burden

The conventional framing of disability inclusion as a compliance exercise misses something important. Designing financial products that work for persons with disabilities does not produce a niche product. It produces a better product for everyone. Voice navigation built for users with visual impairments works equally well for a first-generation smartphone user in a rural area who is more comfortable speaking than typing. High contrast display modes built for users with low vision are easier to read in bright sunlight for any user. Simplified onboarding flows designed to work without complex document handling reduce friction for all users, not just for those with disabilities.

The technology sector calls this the ‘curb cut effect’: Pavement ramps built for wheelchair users end up used constantly by cyclists, delivery workers, and elderly pedestrians alike. Accessibility features built for a specific need routinely improve the experience for a much wider population.

Indian startups are already demonstrating this in practice. PharynxAI has developed real-time sign language detection tools that translate sign language into voice for banking agents, alongside voice-first kiosks for physical bank branches that serve both users with visual impairments and customers with low literacy. SignAble Communications offers real-time Indian Sign Language interpretation for calls and transactions. BarrierBreak has built an entire practice around accessible design for financial and educational institutions.

Voice recognition tools can struggle with non-standard speech patterns, while facial recognition systems may not perform consistently across diverse users.

There are global examples as well. WeBank in China integrated AI-driven speech synthesis to serve customers with visual impairments at scale. Kasikornbank in Thailand combined touch, voice, and vibration systems to serve both people with disabilities and elderly users. True Link Financial in the United States built a financial platform for people with complex needs that the company reports has reached over 150,000 families. In each case, designing for accessibility produced a product with broad market appeal.

These solutions represent meaningful progress, but embedding AI into accessibility features requires careful design and oversight. Voice recognition tools can struggle with non-standard speech patterns, while facial recognition systems may not perform consistently across diverse users. For persons with disabilities, a poorly designed AI feature risks recreating the very exclusion it was intended to eliminate. Co-designing these tools with diverse users and continuously testing them in real-world settings is not optional. It is what separates genuine inclusion from a superficial fix.

India’s fintech sector has demonstrated extraordinary capacity for rapid product innovation. It has not yet turned that capacity toward this problem. The market is large, regulatory momentum is strong, and the technology already exists. What is missing is the recognition that disability inclusion is a market opportunity, not a compliance checkbox.

What needs to happen now

The Supreme Court ruling and the RBI’s follow-through create a window for real change. Four things need to happen before it closes.

Treat accessibility as a prerequisite: Fintechs need to treat accessibility as a product requirement from the beginning of development, not a feature retrofitted after launch. This means co-designing interfaces with users across the disability spectrum during product development, adopting Web Content Accessibility Guidelines (the global standard for making digital content usable for people with disabilities) and Bureau of Indian Standards IS 17802:2021 as baseline requirements, and ensuring that apps incompatible with screen readers or voice navigation do not pass internal quality checks, let alone reach the market.

Reform the video-based identity verification framework: Alternative verification methods that do not require blinking, document display, or verbal responses need formal recognition. Backend identity verification through government-linked data systems can replace document display requirements for many users. Gesture-based and voice-based authentication need regulatory sanction as equivalent alternatives, not workarounds. Caregivers assisting users through onboarding need a formal digital consent framework that protects user autonomy and institutional compliance simultaneously.

Make audits frequent and visible: The sector needs visibility into its own performance. Currently, as the FACE framework submission notes, there is no public disclosure requirement for accessibility compliance, no standardised audit process, and no way for a user with a disability to compare platforms on how well they actually work with assistive technologies. An accessibility scorecard or rating system, voluntary initially and mandatory over time, would create market pressure that moves faster than regulatory enforcement alone.

Embed digital financial accessibility into the development agenda: Civil society organisations and corporate social responsibility (CSR) programmes working on livelihoods or economic empowerment need to treat digital financial accessibility as part of their mandate. When a livelihood programme trains a person with disability and then connects them to a payment system they cannot use independently, the programme has not completed its job. Practitioners can require fintech partners to demonstrate accessibility compliance, include persons with disabilities in user testing, and document barriers that the communities they work with encounter. This is an accountability role the development sector is well placed to play.

India built a financial infrastructure that the world studies and tries to replicate. The question now is whether that same ambition will extend to the tens of millions who have watched this revolution from the outside, because nobody designed it with them in mind.

—

Know more

- Learn more about the current state of digital accessibility in Indian banking.

- Read the RBI’s guidelines on digital payment access for persons with disabilities.

- Read this article on how banks can enable women’s financial inclusion.